The Financial Architecture and Functioning of the EU’s €90 Billion Ukraine Loan

Vol. 21, No. 13 (2026) · Article 937

- The European Union has established a €90 billion Ukraine support loan for the period 2026–2027 to address wartime financing needs and support longer-term stabilization.

- The structure does not constitute a conventional lending operation: EU-level joint funding and debt management are institutionally separated from the on-lending of resources to Ukraine.

- Financing is secured through unified capital market issuances, with proceeds pooled in a central funding framework and subsequently allocated across programmes, ensuring that investors bear EU risk rather than Ukrainian credit risk.

- Principal repayment is event-based and not subject to a predetermined schedule, while interest and refinancing obligations are serviced from the EU budget, creating an indirect fiscal burden for Member States.

- The primary risk of the arrangement lies not in immediate principal losses, but in the sustained cost of interest and refinancing, as well as the uncertainty surrounding reparation inflows, which may, over time, contribute to a deepening of the EU’s fiscal integration through technical means.

In recent years, the European Union has supported Ukraine through a series of interlinked financing instruments aimed at maintaining macroeconomic stability and ensuring the continued functioning of the state. As a next step, the Union has established a €90 billion Ukraine support loan facility (Ukraine Support Loan) for the period 2026–2027, which, beyond sustaining these objectives, is also intended to address longer-term financing needs and support reconstruction.

The purpose of this study is to provide a detailed analysis of the technical functioning of this €90 billion financing arrangement. It examines, on the one hand, how the European Union mobilizes resources from international capital markets to finance lending operations, and, on the other hand, how these resources are channelled to Ukraine through specific mechanisms and conditional frameworks. The analysis also covers the structure of repayment, as well as the sustainability of the Union’s funding model. In addition, it addresses key structural features of the arrangement, including interest cost allocation, the potential non-repayment of principal, and the mechanics of refinancing.

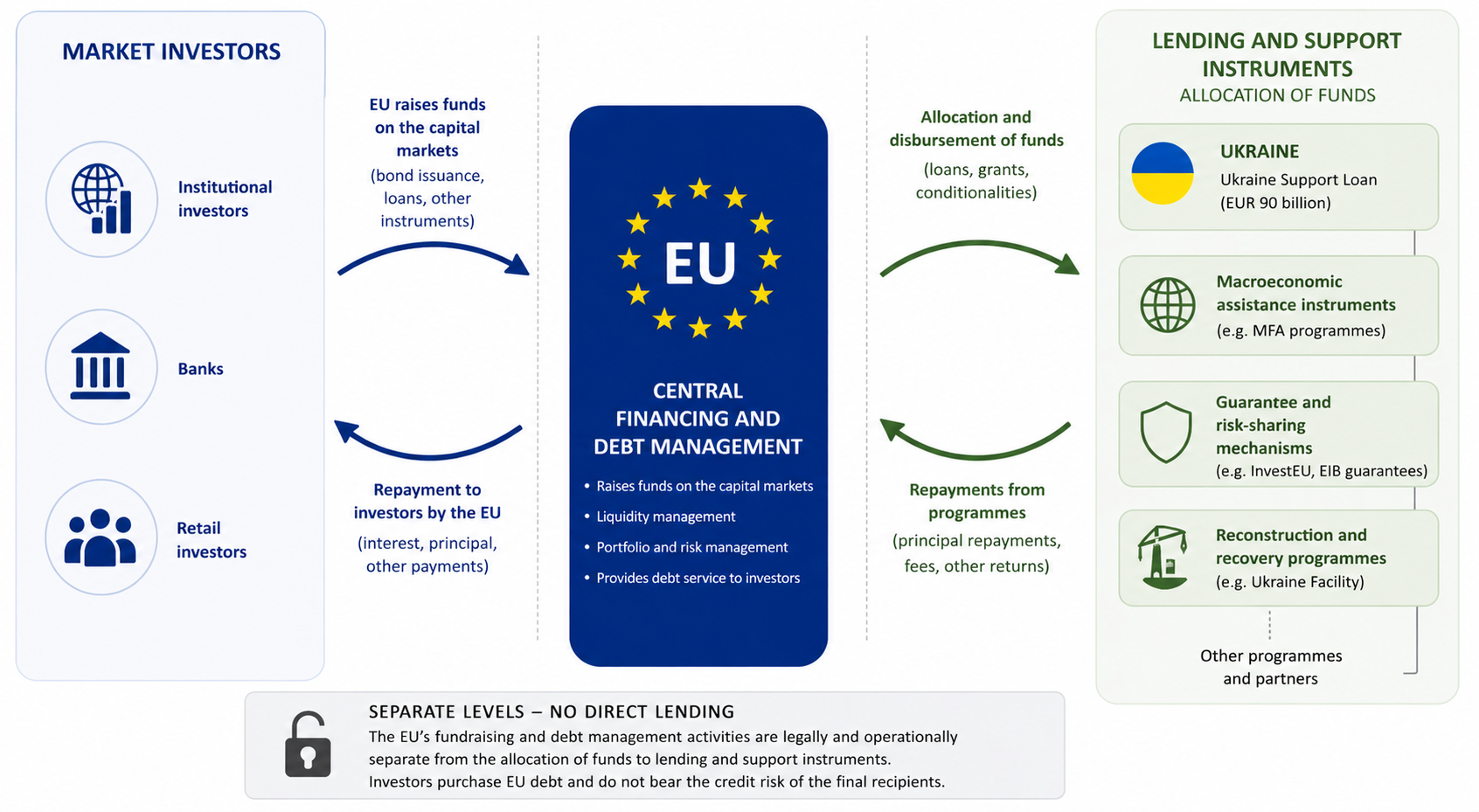

The analysis places particular emphasis on the fact that the arrangement does not constitute a conventional lending operation, but rather rests on a dual structure: EU-level joint funding and debt management on the one hand, and a structurally separate on-lending mechanism to Ukraine on the other.

The full text of the loan agreement is not currently available in public sources. As a result, several operational aspects—such as the precise cash-flow accounting or the administrative mechanics of interest subsidies—can only be partially reconstructed from the available documentation. Nevertheless, the key elements and underlying logic of the process can be reliably inferred from existing sources (European Commission, 2026a; European Parliament and Council, 2026; Council of the EU, 2026a).

1. Fundamentals of the Ukraine Support Loan

The financing of the Ukraine Support Loan is not based on bilateral loans from Member States, but on joint EU-level capital market funding. The structure builds on the borrowing infrastructure and techniques that have been gradually developed over the past decade and a half, drawing on accumulated market experience. Following the 2010 financial crisis, EU borrowing practices took shape through instruments such as the European Stability Mechanism, Macro-Financial Assistance, the Balance of Payments Facility, NextGenerationEU, SURE, and more recently, common defence financing initiatives (ReArm).

Formally, the arrangement is a loan; however, in its financial logic, elements of support and risk-sharing are considerably stronger than in earlier macro-financial assistance instruments. Under the programme, funds are made available in 2026–2027, while the maturity of the underlying EU debt—depending on the structure of bond issuances—extends well beyond this period. As a general rule, principal repayment becomes due only when Ukraine receives war reparations from Russia. The structure of financing thus not only provides liquidity support, but also enables a temporal reconfiguration of repayment obligations. The EU finances, through short- and medium-term market borrowing, a claim whose principal repayment is not based on a fixed schedule, but rather on contingent events linked to the evolution of the reparations process.

As a result, traditional credit risk is effectively shifted away from the market and onto the EU’s budgetary and refinancing framework. Interest and other debt-service obligations vis-à-vis investors are borne by the EU budget, while, in Ukraine’s case, these costs may be partially or fully covered through interest subsidies (European Commission, 2026b; European Parliament and Council, 2026; European Parliament, 2026).

The programme is implemented under the framework of enhanced cooperation within the European Union, allowing a group of Member States to proceed collectively while others may opt out. Expenditures arising from the programme—particularly debt-service costs and the activation of guarantees—are financed from the adopted EU budget and ultimately borne by participating Member States. In contrast, non-participating Member States are subject to internal budgetary adjustments, such as reduced contributions, rebates, or allocation corrections.

The financial effects of the arrangement thus materialize not through national public debt, but through the EU budget’s internal burden-sharing mechanisms. This distinction is essential for understanding that, while the financing is formally not classified as Member State debt, the underlying costs are ultimately borne collectively by the Member States (European Commission, 2026b; European Parliament and Council, 2026; Council of the EU, 2026a).

The analytical part of the study is structured into four main components:

- the EU’s capital market borrowing, examining the institutional and market mechanisms of common bond issuance;

- the on-lending of funds to Ukraine, analysing the legal and financial structure of allocation;

- Ukraine’s repayment mechanism, focusing on event-based principal repayment and its conditionality;

- the debt servicing of EU bonds, addressing the budgetary handling of interest and other payment obligations.

This is followed by a separate chapter examining the risks associated with the structure, as well as the implications for implicit fiscal integration within the EU.

The Lending Structure of the European Union

2. The Structure and Techniques of Lending

2.1. The EU’s Capital Market Borrowing

The legal basis for the programme’s financing is provided by Article 24 of Regulation 2026/467, which authorizes the European Commission, acting on behalf of the European Union, to raise the necessary funds in euro on capital markets or from financial institutions within the framework of a diversified funding strategy as defined in the Financial Regulation. The financing arrangement is implemented through the unified funding system introduced in 2023: the Commission issues uniformly labelled EU bonds, pools the proceeds in a central funding framework, and subsequently allocates resources across individual programmes. In other words, lending is not carried out through earmarked issuances or a direct funding-to-disbursement structure. By relying on this model, the EU ensures that investors assume EU credit risk rather than Ukrainian credit risk (European Parliament and Council, 2026; European Commission, 2026a; European Commission, 2025a).

The issuance process consists of several sequential decision points. First, an annual borrowing ceiling is established, which limits the total volume of short- and long-term funding that the Commission may raise within a given year, including constraints on average maturity and individual issuance volumes. This is followed by the adoption of a semi-annual funding plan, which sets out the indicative issuance calendar for the next six months, including expected volumes, the number of syndicated transactions and competitive auctions, as well as the issuance schedule for EU Bills. For the first half of 2026, the funding plan envisaged €90 billion in long-term EU bond issuance, to be executed through six auctions and six syndicated transactions, across benchmark maturities ranging from 3 to 30 years, with particular emphasis on 3-, 7-, 10-, and 20-year tenors (European Commission, 2026a; European Commission, 2026e).

The technical issuance toolkit rests on two main pillars.

In syndicated transactions, the Commission works with a consortium of appointed banks. These institutions assess and aggregate investor demand, construct the order book, and allocate the bonds among final investors. Syndications typically involve major international investment banks such as BNP Paribas, Deutsche Bank, and JPMorgan Chase. By April 2026, the Commission had successfully conducted several short- and long-term issuances. In January, it raised a total of €11 billion through a €6 billion issuance of a three-year bond maturing in July 2029 and a €5 billion issuance of a thirty-year bond maturing in October 2055. In February, an additional €11 billion was raised through bonds maturing in 2032 and 2045, followed in April by a €9 billion issuance combining a bond maturing in 2029 with a twenty-year bond maturing in 2046. The parallel use of short- and long-term instruments allows the Commission to maintain liquidity across different time horizons (European Commission, 2026f; European Commission, 2026g; European Commission, 2026h).

Competitive auctions constitute an equally important channel. The EU bond auction system in the first half of 2026 typically involved multi-line auctions, offering several bond series simultaneously. In each auction, three different maturities were issued in parallel. Auctions may be followed by a next-day tap allocation, allowing primary dealers—banks contractually linked to the EU and involved in issuance operations—to purchase additional amounts of up to 20% of the original volume at the auction price without further competition. For example, the auction of 27 April 2026 offered three bond lines: a 2.50% bond maturing in December 2031, a 3.25% bond maturing in December 2036, and a 4.00% bond maturing in April 2044, with a total volume of up to €7 billion (European Commission, 2026i; European Commission, 2026j; European Commission, 2026e).

The investor base is broad and composed primarily of stable institutional actors. The Commission relies on a Primary Dealer Network which, as of 9 June 2025, included leading banks from France, Germany, Spain, Italy, the United States, and the Nordic countries. These institutions perform a dual function: they provide direct access to primary issuance through auctions and syndications, and they support secondary market liquidity by continuously quoting buy and sell prices on electronic trading platforms.

Settlement infrastructure has also undergone significant modernization. Since January 2024, all new EU and Euratom bond issuances have been settled through the EU Issuance Service, enabling transactions to be cleared directly via the TARGET2-Securities platform (European Commission, 2024).

Proceeds from bond issuance are not linked to specific programmes, including the Ukraine Support Loan, but are instead pooled within a central funding framework. Under the unified funding approach, different policy programmes are financed from this common pool, with resources allocated internally according to policy needs.

In addition to this central funding pool, the Commission maintains a liquidity buffer. According to the mid-term debt management report, liquid assets amounted to €65.2 billion at the end of 2025, partly to pre-finance the high disbursement volumes expected in 2026 (European Commission, 2026c; European Commission, 2021; European Commission, 2026a).

To estimate financing costs, the Commission applies a cost allocation methodology that distinguishes between funding costs, liquidity management costs, and administrative expenditures. Based on reports for the second half of 2025, the average funding cost for the NextGenerationEU programme stood at approximately 3.32%. However, actual costs varied across programmes: around 2.76% for the Ukraine Facility, 2.54% for macro-financial assistance linked to the Extraordinary Revenue Acceleration (ERA) initiative, and generally between 2.7% and 2.8% for other programmes. The effective cost of the new €90 billion loan will depend on the composition and timing of issuances, as well as programme-level cost allocation. Nevertheless, a range of 2.5% to 4.0% represents a realistic estimate under the 2026 yield environment (European Commission, 2026c).

A key budgetary feature of the arrangement is the absence of a dedicated provisioning reserve for exceptional risks. The regulation explicitly excludes the use of the External Action Guarantee, does not require provisioning, and does not define a provisioning rate. Instead, the legal backstop is provided by the EU budgetary headroom. According to the Commission’s proposal, this headroom underpins the €90 billion borrowing operation, while debt service costs are covered through a newly established instrument— the Ukraine Loan Instrument—mobilized above the standard budgetary ceilings. The programme thus affects Member State budgets indirectly: cost-sharing operates through the EU budget and the internal contribution mechanisms associated with enhanced cooperation, rather than through direct national debt (European Parliament and Council, 2026; European Commission, 2026b; European Commission, 2024).

2.2. On-Lending to Ukraine

The €90 billion envelope does not become available in a single tranche, but is deployed through a sequence of decision and disbursement stages. The first Council implementing decision for 2026 made €45 billion available to cover financing needs until 31 December 2026, of which €16.7 billion is allocated to budgetary support and €28.3 billion to the development of defence-industrial capacities. Within the €16.7 billion envelope, €8.35 billion is channelled through the lending window, while the remaining €8.35 billion takes the form of macro-financial assistance under Regulation 2026/467. The annual utilization of the €90 billion framework depends on the adoption of Council implementing decisions; disbursement is therefore not automatic but subject to annual approvals (Council of the EU, 2026a; European Parliament and Council, 2026).

Disbursements under the budgetary support pillar are carried out in multiple steps. Under the regulatory framework, Ukraine may submit duly justified requests for funds—generally up to six times per year. In the case of macro-financial assistance, each request must be accompanied by reporting under the Memorandum of Understanding (MoU). The Commission may authorize disbursement only if three sets of conditions are met simultaneously: the democratic and rule-of-law preconditions set out in Article 5 of Regulation 2026/467, the policy conditionality defined in the MoU, and the obligations stipulated in the Ukraine Support Loan Agreement. The 2026 macro-financial envelope may be disbursed in up to three instalments, indicatively in amounts of €3.2 billion, €3.7 billion, and €1.45 billion (European Parliament and Council, 2026; Council of the EU, 2026a).

The defence-industrial lending component is subject to an even more tightly controlled disbursement regime. Each funding request must be supported by a contract or agreement, together with an associated implementation schedule. Where the requested amount exceeds 20% of the annual allocation set by the relevant Council implementing decision, Ukraine is required to provide detailed justification regarding the impact on subsequent requests. Upon a positive decision by the Commission, disbursements are capped at the value of the submitted contracts. Consequently, defence-related payments do not constitute general liquidity transfers but take the form of contract-based, invoiced, and verifiable expenditures (European Parliament and Council, 2026).

The financial flows within the defence pillar are subject to particularly stringent controls. Ukraine must establish a dedicated account exclusively for the management of these funds, from which all related contractual payments are to be executed. The Commission is granted oversight rights over this account, and Ukraine is required to submit monthly reports within ten working days after the end of each month, specifying the date, amount, beneficiary, and contractual purpose of each payment (European Parliament and Council, 2026). In addition to contractual and accounting safeguards, the framework incorporates industrial policy and security filters. The regulation stipulates that, in the case of defence products, the cost share of components originating outside the EU, the EEA EFTA states, and Ukraine may not exceed 35%. Public procurement and contracting procedures must also align with the security and defence interests of the Union and its Member States (European Parliament and Council, 2026).

Disbursement is conditional upon the availability of the required guarantee coverage for the given year. The Council implementing decision of April 2026 explicitly states that the €45 billion envelope cannot be disbursed until the guarantee framework is in place. This requirement is critical, as the operational launch of the programme depends not only on political authorization but also on the effective availability of the underlying budgetary backstop (Council of the EU, 2026a; European Commission, 2026a).

An additional element of the loan security structure is that, according to the public proposal, the Ukraine Support Loan Agreement must establish a security interest in favour of the EU over Ukraine’s claims for reparations against Russia. The final regulation requires this as a mandatory component of the loan agreement. Based on the available information, the EU is not merely relying on the prospect of future reparations, but seeks—within the limits of what is feasible in the context of sovereign war-related claims—to legally collateralize such claims. The precise legal structure of this security arrangement, however, is set out in the loan agreement, which is not publicly available (European Commission, 2026b; European Parliament and Council, 2026).

2.3. Ukraine’s Repayment System and Conditionality

As a general rule, Ukraine repays the loan in instalments. While such payments may, in principle, include both principal and interest components, principal repayment arises only on a conditional basis, triggered by the occurrence of specified events.

The central element of the repayment mechanism is the set of repayment triggers. Under the regulation, Ukraine’s obligation to repay principal arises within 30 days if it receives war reparations, compensation, or financial settlement from Russia in cash. If compensation is received in non-monetary form—excluding territorial transfers—repayment is generally due within 90 days, based on an independent valuation; the Commission may grant a limited extension in duly justified cases. Additional triggers include breaches of democratic and rule-of-law conditions, as well as the detection of fraud, corruption, or other illegal activities affecting the financial interests of the Union. In cases of contractual breach, the full outstanding amount may become immediately due, while in cases of fraud or corruption, at least the affected portion becomes immediately payable (European Parliament and Council, 2026).

The allocation of repayments linked to reparation inflows is defined by a mathematical formula. The proportional allocation is given by:

EU repayment = R × [O_EU / (O_EU + O_G7 + O_ERA)]

where R denotes the value of the reparation inflow or the monetary valuation of a non-cash asset, O_EU is the outstanding amount of the EU’s Ukraine Support Loan, O_G7 represents the outstanding stock of comparable G7 reparation-linked loans, and O_ERA refers to obligations associated with the Extraordinary Revenue Acceleration (ERA) mechanism.

This rule is designed to prevent the entirety of early reparation inflows from being absorbed by the EU alone (European Parliament and Council, 2026).

The operation of this formula can be illustrated with a simple numerical example. Suppose that €90 billion remains outstanding under the EU loan, while G7 reparation-linked loans and ERA-related obligations each amount to €30 billion. If Ukraine receives €20 billion in cash reparations, the EU share would be €20 × 90 / (90 + 30 + 30) = €12 billion, payable within 30 days. If Ukraine receives a non-monetary asset valued at €50 billion, the EU share would amount to €30 billion, generally payable within 90 days. The remaining outstanding EU claim persists until subsequent trigger events occur (European Parliament and Council, 2026).

On the principal side, the loan is thus event-based; on the interest side, however, it formally retains the characteristics of a standard loan. Article 22 of the regulation is crucial for understanding whether Ukraine bears interest costs. According to this provision, the Union may, subject to available resources, cover the financing costs that would otherwise be borne by Ukraine. These costs extend beyond nominal interest to include the cost of funding, liquidity management expenses, and administrative service costs.

Ukraine may request interest subsidies on an annual basis, and the Commission may grant them up to the level of appropriations available in the relevant budgetary procedure. In legal terms, the default allocation of costs lies with Ukraine, but the regulation allows the EU budget to assume these costs through annual subsidy decisions. Public budgetary documents anticipate that these costs will, in practice, be largely or fully covered by the EU (European Parliament and Council, 2026; European Commission, 2026b; European Parliament, 2026).

From this, the structure of interest cost allocation becomes clear. The EU pays interest to investors in all cases. The extent to which Ukraine ultimately bears these costs depends on the level of interest subsidy granted in a given year. Available political and budgetary signals suggest a high or near-complete level of cost absorption by the EU. However, in the absence of the full loan agreement, it cannot be determined with certainty whether interest is first recorded as a claim against Ukraine and subsequently compensated through subsidies, or whether the contractual structure directly incorporates the subsidy mechanism. In economic terms, the outcome is equivalent: the EU budget services the debt vis-à-vis investors, and this constitutes the Union’s net fiscal cost (European Parliament and Council, 2026; European Commission, 2026b).

The repayment framework also includes a politically sensitive component. The regulation preserves the EU’s right to use immobilized Russian assets within the Union for the purpose of loan repayment, in full compliance with EU and international law. While this does not in itself establish a comprehensive confiscation regime, it indicates that the legislator has incorporated the possibility of reparations and asset mobilization into the loan structure from the outset. The practical application of this provision would, however, require further developments in both EU and international law (European Parliament and Council, 2026; Council of the EU, 2026a).

2.4. Debt Servicing of EU Bonds

The legal relationship between the European Union and investors is defined by the terms and conditions of the bond issuances—covering interest payments, principal repayment, maturity structure, and other contractual provisions—rather than by Ukraine’s subsequent repayment capacity. EU bonds (EU-Bonds) are fixed-rate instruments, typically issued at benchmark maturities and generally structured as bullet securities, with coupons paid at predetermined intervals and principal repaid in full at maturity. By contrast, EU Bills are short-term instruments, typically with maturities of 3, 6, or 12 months, primarily used for liquidity management purposes. As a result, the refinancing burden associated with the Ukraine Support Loan is not concentrated at a single point in time, but is instead distributed across the EU’s broader debt portfolio (European Commission, 2026e; European Commission, 2026f; European Commission, 2026h).

The primary source for meeting interest and principal obligations vis-à-vis investors is the Commission’s central treasury and liquidity management. Under the unified funding approach, individual programmes are not financed through earmarked bond issuances, but from a common funding pool. Consequently, when a specific bond matures, the EU does not link repayment to the performance of a particular loan—such as the €90 billion Ukraine Support Loan—but instead determines the mode of repayment at the level of the overall funding portfolio. Payments may thus be made from available cash reserves, through short-term refinancing (via EU Bills), or by issuing new longer-term bonds. This approach aligns the EU’s financing practice with that of sovereign issuers (European Commission, 2026a; European Commission, 2026c).

Within this structure, EU Bills do not serve as primary funding instruments but rather as tools of cash management. The Commission uses short-term securities to smooth its liquidity profile: bi-weekly bill auctions, combined with an adequate cash buffer, allow large coupon and redemption payments to be managed without relying exclusively on long-term bond issuance timed to specific dates. At the end of 2025, the stock of EU Bills amounted to €36.8 billion, while liquid assets totalled €65.2 billion, indicating that the Commission manages forthcoming disbursement peaks in 2026 from a portfolio perspective. One practical implication is that the financial risk associated with the Ukraine Support Loan manifests primarily as refinancing and interest rate risk on the market side, rather than as immediate liquidity risk (European Commission, 2026c).

A key practical question concerns the situation in which an EU bond matures before Ukraine’s principal repayment becomes due, or where repayment has become due but has not been received. The available regulatory framework implies two main financing channels. The first is rollover through new issuance: the Commission replaces maturing securities by issuing new EU bonds or, for shorter bridging periods, EU Bills. The second pillar is the EU budgetary backstop: debt service obligations, and where necessary the activation of guarantees, can be covered through the adopted budget and, if required, through special instruments mobilized above standard budgetary ceilings. Internal adjustments among non-participating Member States do not affect the market-facing structure: vis-à-vis investors, the issuer remains the European Union as a single entity (European Commission, 2026b; European Parliament and Council, 2026; Council of the EU, 2026a).

The lending operation entails direct costs for the Union. Unlike a conventional market-based lending transaction, where the lender generates a margin on interest, a portion of the financing costs in this case is borne by the EU budget, potentially resulting in a net fiscal burden. Assuming an average funding cost of 3.0% applied to a fully drawn €90 billion stock, the steady-state annual interest and liquidity cost amounts to approximately €2.7 billion. This figure is broadly consistent with the European Parliament’s estimate of around €3 billion per year from 2028 onwards. While this cost does not appear as national public debt, it is reflected in the EU’s annual budget. Interest payments to investors are financed from the budget, and these debt-service costs constitute the direct net fiscal burden of the programme for the Union (European Commission, 2026b; European Parliament, 2026).

The evolution of financing costs is fundamentally determined by the level of interest rates. Higher market yields increase annual costs both through new issuances and through refinancing operations. Starting from the Commission’s official estimate of approximately €1 billion for 2027, and assuming a fully drawn €90 billion stock from 2028 onwards, the annual cost varies significantly across different rate scenarios. At a 2.5% funding rate, annual costs are approximately €2.25 billion; at 3.0%, €2.7 billion; at 3.5%, €3.15 billion; and at 4.0%, €3.6 billion. Over longer horizons, these differences accumulate substantially: by 2035, total costs range from around €19 billion at lower rates to €26–30 billion under higher-rate scenarios, while by 2045 the range broadens to approximately €41–66 billion. A 100 basis point increase in the yield environment translates into an additional annual cost of roughly €0.9 billion for a fully drawn portfolio. This is consistent with the Commission’s own sensitivity analysis, which indicates that appropriations for 2027 could increase to as much as €1.3 billion under a 100 basis point interest rate shock (European Commission, 2026b; European Parliament, 2026).

3. Risks

The risk analysis examines the expected cost and exposure dynamics of the lending structure under different scenarios. In the baseline scenario, reparation inflows begin in 2032 and gradually lead to the full repayment of the €90 billion principal. In a delayed scenario, inflows only commence in the late 2030s, resulting in partial recovery by 2045. In the no-reparations scenario, the full principal exposure remains on the EU’s balance sheet over the long term. Across all three cases, the interest rate path is held constant, so differences are driven primarily by the timing of inflows (European Parliament and Council, 2026; European Commission, 2026b).

In the short and medium term, the cost dynamics of the structure are determined not by principal loss, but by the burden of interest and refinancing. Costs do not arise as a one-off loss, but as a continuous stream: the EU must service interest payments and roll over maturing debt year after year. The timing of reparation inflows is therefore critical. Early inflows can reduce refinancing pressure, whereas delayed or absent inflows do not materially alter the overall risk trajectory (European Commission, 2026c).

In the most restrictive scenario—where no reparations materialize—the cumulative interest burden over a twenty-year horizon approaches €50 billion, while the full €90 billion principal exposure remains outstanding. This does not appear as a single loss event, but as an ongoing burden financed through the EU’s common debt management system. The essence of the structure lies precisely in this feature: fiscal exposure materializes through a sequence of interest payments and refinancing operations, which may be more manageable politically, but nonetheless represent a real economic cost (European Commission, 2026b; European Commission, 2026c).

The main market risk relates to the level of interest rates. A 100 basis point increase in the funding rate could generate an additional annual cost of approximately €0.9 billion for a fully drawn portfolio, in line with the Commission’s own sensitivity estimates. Interest rate risk therefore materializes directly at the level of the EU budget (European Commission, 2026b).

Legal and political risks stem from the conditional nature of the repayment framework. The structure relies on future reparation flows and the potential mobilization of assets, both of which remain institutionally and legally uncertain. If these mechanisms do not materialize, the loan may gradually evolve into a persistent, budget-supported EU refinancing facility. This, in turn, creates a precedent: the combination of joint issuance, common debt management, and shared cost-bearing reinforces the technical instruments of fiscal integration. Even in the absence of formal institutional reform, the arrangement effectively extends the practical boundaries of EU fiscal integration (European Commission, 2026a; European Parliament, 2026; European Parliamentary Research Service, 2026).

4. Conclusions

The €90 billion Ukraine Support Loan represents one of the most complex constructs in EU financial law. It simultaneously functions as a loan, a form of joint debt issuance backed by the EU budget, an instrument of industrial policy, and a financing mechanism linked to future reparation claims.

At its core, the programme leverages the EU’s now well-developed and liquid capital market infrastructure to support Ukraine’s financing needs, while decoupling the timing and source of principal repayment from market-based funding. The EU assumes full responsibility for servicing obligations vis-à-vis investors, whereas Ukraine’s principal repayment remains contingent on uncertain future events. This separation constitutes both the fundamental strength of the arrangement and one of its principal sources of risk (European Commission, 2026a; European Parliament and Council, 2026; European Commission, 2026c).

From the perspective of net EU costs, the key finding is that debt service—comprising interest payments, liquidity management, issuance costs, and administrative expenditures—is borne by the EU budget. Member States do not incur these obligations as national public debt; instead, they contribute indirectly through the EU budget’s contribution mechanisms and the system of special instruments. While the classification of the operation as a “non-Member State loan” is legally accurate, its fiscal effects ultimately materialize at the level of participating Member States, as the burden of interest payments and refinancing obligations is effectively shared among them (European Commission, 2026b; European Parliament and Council, 2026).

From a policy perspective, the programme points in two directions. In the short term, it provides a rational response to Ukraine’s exceptional financing needs, as the EU is better positioned than Ukraine to manage market access and refinancing risks. Over the longer term, however, the sustainability and political legitimacy of the arrangement depend on how the EU addresses the post-2028 budgetary framework, whether it establishes transparent rules for the annual allocation of financing cost support, and how it defines the ultimate budgetary response in the event of non-repayment of principal. In the absence of such clarification, the loan risks evolving into a permanent mechanism of shared fiscal burden (European Parliament, 2026; European Parliamentary Research Service, 2026; European Commission, 2026b).

A major limitation of the present analysis is the absence of the full text of the Ukraine Support Loan Agreement and the associated Memorandum of Understanding. As a result, key operational aspects—such as the detailed mechanics of interest subsidies, the precise cash-flow pathways of repayments, the legal structure of collateral arrangements, and the principles governing the use of principal inflows for maturity management—cannot be fully reconstructed. These elements are of central importance for both the constitutional and fiscal assessment of the programme, and their future publication may require a refinement of some of the conclusions presented here.

References

- Council of the European Union (2026a) Proposal for a Council Implementing Decision approving assistance to Ukraine in implementing the Ukrainian Financing Strategy.

- European Commission (2021) Communication on the financing strategy for NextGenerationEU.

- European Commission (2024) European Commission settles first transaction via new Eurosystem-based EU Issuance Service.

- European Commission (2025a) Funding plan January–June 2026.

- European Commission (2026a) Commission presents a financial support package for Ukraine for 2026–2027.

- European Commission (2026b) Proposal for a Regulation implementing enhanced cooperation on the establishment of the Ukraine Support Loan for 2026 and 2027.

- European Commission (2026c) Half-yearly report on the implementation of borrowing, debt management and related lending operations.

- European Commission (2026e) How EU issuance works.

- European Parliament (2026) Parliament approves €90 billion Ukraine support loan package.

- European Parliament and Council (2026) Regulation (EU) 2026/467 implementing enhanced cooperation on the establishment of the Ukraine Support Loan for 2026 and 2027.

- European Parliamentary Research Service (2026) EU support for Ukraine for 2026–2027.

- International Monetary Fund (2026) Ukraine: Request for an Extended Arrangement under the Extended Fund Facility and related Board materials.